From Surf Wiki (app.surf) — the open knowledge base

Risk premium

Measure of excess

Measure of excess

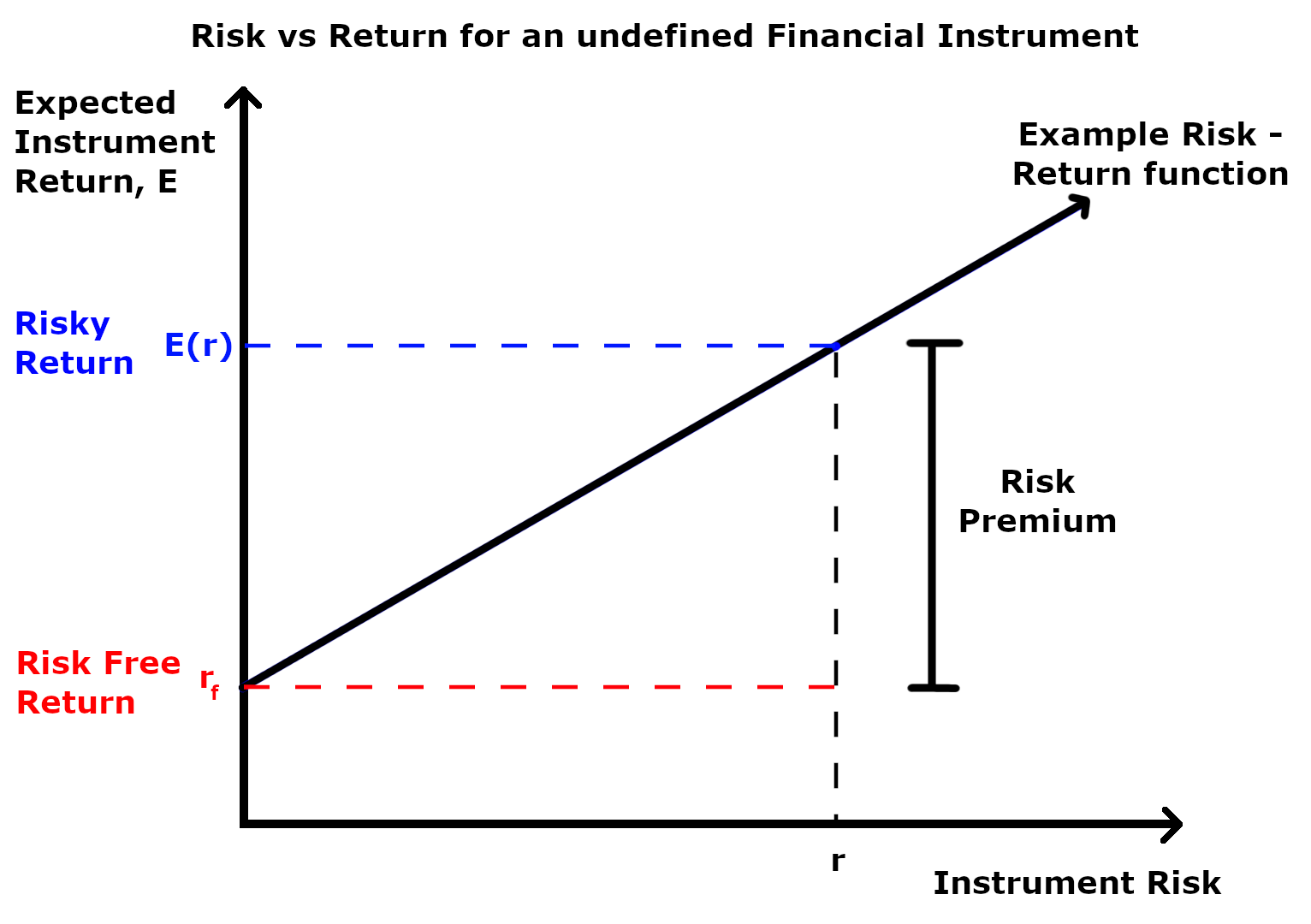

A risk premium is a measure of excess return that is required by an individual to compensate being subjected to an increased level of risk. It is used widely in finance and economics, the general definition being the expected risky return less the risk-free return, as demonstrated by the formula below.

Risk \ premium = E(r) - r_f

Where E(r) is the risky expected rate of return and r_f is the risk-free return.

The inputs for each of these variables and the ultimate interpretation of the risk premium value differs depending on the application as explained in the following sections. Regardless of the application, the market premium can be volatile as both comprising variables can be impacted independent of each other by both cyclical and abrupt changes. This means that the market premium is dynamic in nature and ever-changing. Additionally, a general observation regardless of application is that the risk premium is larger during economic downturns and during periods of increased uncertainty.

There are many forms of risk such as financial risk, physical risk, and reputation risk. The concept of risk premium can be applied to all these risks and the expected payoff from these risks can be determined if the risk premium can be quantified. In the equity market, the riskiness of a stock can be estimated by the magnitude of the standard deviation from the mean. If for example the price of two different stocks were plotted over a year and an average trend line added for each, the stock whose price varies more dramatically about the mean is considered the riskier stock. Investors also analyse many other factors about a company that may influence its risk such as industry volatility, cash flows, debt, and other market threats.

Formal definition in expected utility theory

In expected utility theory, a rational agent has a utility function that maps sure-outcomes to numerical values, and the agent ranks gambles over sure-outcomes by their expected utilities.

Let the set of possible wealth-levels be \R. A gamble Z is a real-valued random variable. The actuarial value of the gamble is just its expectation: \mathbb E [Z]. This is independent of any agent.

Let the agent have a utility function u: \R \to \R, with a wealth-level w\in \R. The risk-premium of Z for the agent at wealth-level w is \pi(w, Z), defined as the solution tou(w + \mathbb E[Z] - \pi) = \mathbb E [u(w + Z)].

Note that the risk-premium depends both on the gamble itself, the agent's utility function, and the wealth-level of the agent. This can be understood intuitively by considering a real gamble. Some people may be quite willing to take the gamble and thus have a low risk-premium, while others are more averse. Further, as one's wealth increases, one is usually less perturbed by the gamble, whose stakes diminishes relative to one's wealth, consequently the risk-premium \pi(w, Z) often decreases as w increases, holding Z constant.

In public goods

In invasive species management

The option value of whether to invest in invasive species quarantine and/or management is a risk premium in some models.

In agriculture

Of crop pathogens

Farmers cope with crop pathogen risks and losses in various ways, mostly by trading off between management methods and pricing that includes risk premiums. For example in the northern United States, Fusarium head blight is a constant problem. Then in 2000 the release of a multiply-resistant cultivar of wheat dramatically reduced the necessary risk premium. The total planted area of MR wheats was dramatically expanded, due to this essentially costless tradeoff to the new cultivar.

Of investment in genetic research

Estimates of costs of research and development - including patent costs - of new crop genes and other agricultural biotechnologies must include the risk premium of those which do not ultimately obtain patent approval.

References

References

- (2016). "Time-Varying Risk Premium in Large Cross-Sectional Equity Data Sets". Econometrica.

- (2020). "Recovering the market risk premium from higher-order moment risks". European Financial Management.

- (October 2015). "The Equity Risk Premium in 2015".

- Kenton, Will. "Risk Management in Finance".

- Pratt, John W.. (1964). "Risk Aversion in the Small and in the Large". Econometrica.

- (2003). "Estimating the stock/bond risk premium". Journal of Portfolio Management.

- (1993). "The market risk premium and long-term stock returns". Journal of Portfolio Management.

- (2019). "Assessing Risk Aversion From the Investor's Point of View". Frontiers in Psychology.

- (2016). "Credit spread variability in the U.S. business cycle: The Great Moderation versus the Great Recession". Journal of Banking & Finance.

- (2013). "New Zealand finance companies and risk premiums". Accounting & Finance.

- Adusei, Michael. (2019). "The finance–growth nexus: Does risk premium matter?". International Journal of Finance and Economics.

- Danthine, Jean-Pierre.. (2015). "Intermediate financial theory". Elsevier/Academic Press.

- McClure, Ben. "Explaining The Capital Asset Pricing Model (CAPM)".

- (2018). "Downside Risk Aversion and the Downside Risk Premium". The Journal of Risk and Insurance.

- Olson, Craig A.. (1981). "An Analysis of Wage Differentials Received by Workers on Dangerous Jobs". The Journal of Human Resources.

- (1983). "Wage-Risk Premiums and Workers' Compensation: A Refinement of Estimates of Compensating Wage Differential". The Journal of Political Economy.

- (2017). "Career choice and the risk premium in the labor market". Review of Economic Dynamics.

- Hagen, Tobias. (2003). "Do Temporary Workers Receive Risk Premiums? Assessing the Wage Effects of Fixed–term Contracts in West Germany by a Matching Estimator Compared with Parametric Approaches". Labour.

- (2012). "The Executive Turnover Risk Premium". SSRN Electronic Journal.

- (2002). "Management Turnover Across the Corporate Hierarchy". SSRN Electronic Journal.

- (2010). "Invasive Species and Endogenous Risk". [[Annual Reviews (publisher).

- (2019). "Breeding wheat for resistance to Fusarium head blight in the Global North: China, USA, and Canada". [[Crop Science Society of China]] ([[Elsevier]]).

- (2002). "Patenting Genes and Genetic Research Tools: Good or Bad for Innovation?". [[Annual Reviews (publisher).

- {{cite Q. Q106644168.

This article was imported from Wikipedia and is available under the Creative Commons Attribution-ShareAlike 4.0 License. Content has been adapted to SurfDoc format. Original contributors can be found on the article history page.

Ask Mako anything about Risk premium — get instant answers, deeper analysis, and related topics.

Research with MakoFree with your Surf account

Create a free account to save articles, ask Mako questions, and organize your research.

Sign up freeThis content may have been generated or modified by AI. CloudSurf Software LLC is not responsible for the accuracy, completeness, or reliability of AI-generated content. Always verify important information from primary sources.

Report